Oops! Something went wrong while submitting the form.

Glossary

A repository of acronyms, jargon, and useful definitions perfect for eCommerce founders & marketers like yourself.

Glossary

>

M

>

Mix Effect

Mix Effect

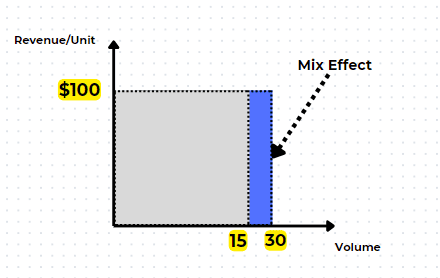

Mix-effect measures the impact on the sales amount resulting from a change in the mix of quantities sold.

With mix-effect, even by keeping the total quantities and prices the same, sales can increase if we sell a higher proportion of expensive products.

It is calculated as the difference between the actual unit and the actual unit at budget price multiplied by the budget price.

For example, if we calculate the mix-effect for any product where the actual unit is 30 and the actual unit at a budget price is 15, then:

Mix effect on quantities 30-15= 15 units.

In this case:

Mix effect= Mix effect on quantities x budget price = 15 x 100 = 1500 EUR

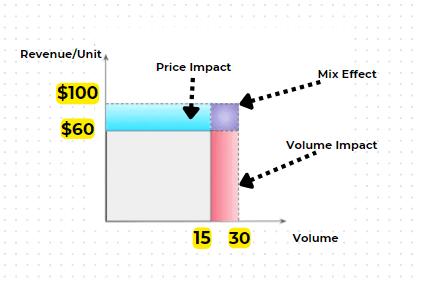

Price Volume Mix Analysis has the following three components

Price Impact (applying higher or lower selling prices per unit)= Target Volume * (Actual price - Target price)

Volume Impact (variation in the number of units sold)= Target Price * (Actual volume - Target volume)

Mix Impact (change in the mix of quantities sold)= (Actual volume - Target volume) * (Actual price - Target price)

Why measure the mix effect?

Diagnostic purpose: Mix effect and price can explain changes in margin and sales

Performance management: If new products or investing in marketing is supposed to improve the mix, then these KPIs can be used to evaluate performance and set the target in advance

Benefits of PVM analysis

Standardizing your Price-Volume-Mix assessment: Tracking the reason for cost increments can be difficult, yet distinguishing causality is critical for your association's drawn-out development. PVM is proposed to assist you with recognizing and conveying the changes to your C-suite associates by empowering you to bore down into the subtleties. In businesses where unstable costs make anticipating profitability harder, you may incorporate a cost bucket and make your PVM assessment on a margin basis

Bridge-building benefits: By identifying and distinguishing the impact of pricing on your revenue or margin and filtering this data by relevant business parameters, you can quantify the adequacy — and inadequacies — of your pricing activities and strategies. The data from the analysis can help you improve your pricing practices and ensure that you are implementing them to get the maximum profit

How To Calculate the Selling Price of a Product From Mix Effect?

Step 1: Calculate the Mix Effect with PVM Analysis:

Use the formula for mix effect: (Actual Units - Target Units) x Budget Price

Analyze it for each product or product category

Identify products with positive and negative mix effects

Example:

Positive mix effect > $1,000: Increase price by 5%

Positive mix effect between $500 and $1,000: Increase price by 3%

Focus on maximizing sales of high-margin products with positive mix effects

Step 4: Analyze Price Sensitivity:

Understand how customers respond to price changes for different products

Use historical data or conduct market research to assess price elasticity

Step 5: Adjust Prices Strategically:

For products with positive mix effects and low price sensitivity: Raise prices to capture more value

For products with negative mix effects and high price sensitivity: Consider lowering prices to stimulate demand

Experiment with bundle offerings or targeted promotions to influence the mix effect

Step 6: Keep The Monitor On:

Track the impact of price changes on revenue, mix effect, and profitability

Adjust prices further based on ongoing analysis and market trends

Use PVM analysis regularly to decompose revenue changes and make informed decisions

Additional Considerations:

Factor in psychological pricing strategies (e.g., charm pricing, price anchoring)

Take good note of competitor pricing and adjust accordingly

Align pricing with inventory levels to avoid stock outs or excess stock

Make sure you don’t adjust pricing based on a category’s mix effect threshold—instead, focus on the mix effect of individual products

Apply appropriate rounding rules to new prices—for example, round up $47.54 to $49.99

Tips For Conducting a Price Volume Mix Analysis

The Blanket Rule: Analyze the variances for each product and timeframe.

Positive values indicate increases in revenue due to that factor (e.g., price increase leading to positive price variance), while negative values indicate decreases.

In case you missed it, PVM Analysis can help find trends and patterns—answer these questions:

“Are certain products driving more price variance”, or are specific periods seeing significant volume or mix effects?

Furthermore, if a product has a high positive price variance, consider raising its price further

Similarly, if another product has negative volume variance, figure out the reasons and adjust its marketing or promotions accordingly

You can further break down the mix variance into “quantity mix” and “price mix” to understand the specific influences within the combined effect

Lastly, PVM can be the make-or-break factor when it comes to price wars

Quick Recap: Easy-to-follow formulas

Mix Effect Formula:

(Actual Units - Target Units) x Budget Price

Price Impact / Price Variance Formula:

(Actual Price - Average Historical Price) x Actual Quantity

Volume Impact / Volume Variance Formula:

(Actual Quantity - Average Historical Quantity) x Average Historical Price

Mix Variance Formula:

Actual Revenue - (Average Historical Quantity x Actual Price)

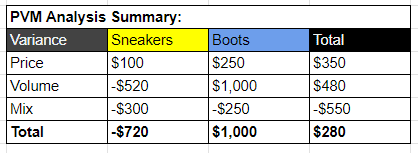

In this example, we have taken two products—Sneakers at $54 MSRP and boots at $105 MSRP.

We'll conduct a PVM analysis for the month of December, comparing it to the historical average prices and volumes from November.

Thus, the PVM Calculations are as follows:

Price Variance:

Sneakers: ($54 - $52) * 50 = $100

Boots: ($105 - $100) * 50 = $250

Total Price Variance: $100 + $250 = $350

Volume Variance:

Sneakers: (50 - 60) * $52 = -$520

Boots: (50 - 40) * $100 = $1,000

Total Volume Variance: -$520 + $1,000 = $480

Mix Variance:

Sneakers: $2,700 - (50 * $54) = -$300

Boots: $5,250 - (50 * $105) = -$250

Total Mix Variance: -$300 - $250 = -$550

Figuring Out The Price Volume Mix Variance Analysis

To calculate profit, we need to consider both revenue and costs. Assuming the cost per unit for sneakers is $30 and for boots is $70, we can calculate:

Total Revenue:

Sneakers: $54 * 50 = $2,700

Boots: $105 * 50 = $5,250

Total Revenue: $2,700 + $5,250 = $7,950

Total Cost:

Sneakers: $30 * 50 = $1,500

Boots: $70 * 50 = $3,500

Total Cost: $1,500 + $3,500 = $5,000

Total Profit:

Total Profit = Total Revenue - Total Cost

Total Profit = $7,950 - $5,000 = $2,950

Calculating Profit From Price Impact / Total Price Variance (TPV):

Formula: TPV = Σ (Actual Price - Average Historical Price) * Actual Quantity

Sneakers: ($54 - $52) * 50 = $100

Boots: ($105 - $100) * 50 = $250

Total Price Variance Profit: $100 + $250 = $350

This means price increases contributed $350 to overall profit.

Calculating Profit From Volume Variance (VVP):

Formula: VVP = Σ (Actual Quantity - Average Historical Quantity) * Average Historical Price

Sneakers: (50 - 60) * $52 = -$600

Boots: (50 - 40) * $100 = $1,000

Total Volume Variance Profit: -$600 + $1,000 = $400

Increased volume for boots contributed $1,000 to profit, but decreased volume for sneakers resulted in a loss of $600, leading to a net gain of $400.

Total Mix Variance Profit: -$300 - $250 = -$550 (matches the provided figure)

The mix variance is negative because the combined effect of price & volume changes for each product resulted in lower revenue than what could have been achieved with simply maintaining historical prices and quantities.

Breakdown of Profit by Variance:

Price Variance Profit: $350

Volume Variance Profit: $400

Mix Variance Profit: -$550

Total Profit: $350 + $400 - $550 = $200

Interpreting The Results

The positive price variance ($350) indicates that price increases contributed to higher revenue

The positive volume variance ($400) suggests that selling more units also boosted revenue

However, the negative mix variance (-$550) means that each product's price and volume changes negatively impacted revenue, suggesting potential shifts in customer preferences or product profitability

While price and volume increases contributed positively to profit, the negative mix effect overshadowed those gains, resulting in a total profit of $200

The store could consider further price increases for boots, as they had a strong positive price variance

Investigate the reasons for the negative mix variance, such as lower-than-expected demand for sneakers or a shift in customer preferences towards boots

Note: These calculations assume a constant cost per unit. For variable costs, adjust the Total Cost formula accordingly.

Mix Effect FAQs

1. What's the difference between price effect and mix effect?

Price effect measures the impact of changing the selling price of the same product, while mix effect measures the impact of changes in the proportion of products sold.

Price effect reflects pricing decisions; mix effect reflects shifts in product demand or customer purchasing behavior.

2. Can mix effect be negative?

Yes. A negative mix effect occurs when customers purchase a greater share of lower-priced or lower-margin products, reducing overall revenue or profitability even if total sales volume remains unchanged.

3. How is mix effect used in Price Volume Mix (PVM) analysis?

Mix effect is one of the three core components of PVM analysis, alongside price effect and volume effect.

Together, these metrics help explain whether changes in revenue are driven by pricing decisions, sales volume, or shifts in the product mix.

Thank you. We'll be in your inbox soon 🙂

Oops! Something went wrong while submitting the form.

x

Find fresh (and proven) ways to instantly improve your product page conversions

.avif)

.svg)

.svg)

.svg)

.svg)